You log into Shopify, check yesterday’s payout, and the number feels wrong.

Sales looked healthy. Orders came in. Conversion held up. Then the payout lands, and the gap between top-line revenue and what hits your account is bigger than you expected. That’s where a lot of merchants wake up to shopify cc fees. Not when they read the pricing page, but when cash lands short.

I’ve seen this across hundreds of eCommerce P&Ls. Founders obsess over ad costs, discounting, and shipping, then treat payment fees like a fixed tax they can’t control. That’s a mistake. Card fees aren’t just an accounting line. They change your profit per order, your pricing flexibility, and your ability to scale paid acquisition without choking margin.

The right question isn’t “What does Shopify charge?” The right question is “What does each order leave me after fees, and which levers improve that number fastest?” That’s the lens that matters.

What You Really Pay Shopify for Each Sale

The most common misunderstanding is thinking the advertised card rate is the whole story. It isn’t.

A merchant sees an online rate on their plan, assumes that’s the cost of taking payment, and moves on. Then the monthly P&L shows a bigger drag than expected because the actual cost picture includes more than the card swipe itself. Subscription fees, payment processing, and other direct platform costs all stack together.

According to merchant cost analysis from IRP Commerce, when all direct platform costs are included, Shopify fees typically land between 3% and 5% of sales, with a median average of 3.5%. The same analysis says a store doing $5,000 per month pays about $240 in total platform fees, or 4.8% of revenue, while a store doing $100,000 per month pays about $3,550, or 3.5% of revenue.

That range matters because margin is won or lost in the spread between revenue and contribution profit. If you sell a product with healthy gross margin, sloppy fee management is annoying. If you sell a product with tight margin, sloppy fee management can wipe out your room to advertise.

Why payout shock happens

Most merchants don’t feel the pain on one order. They feel it in aggregate.

You run a promo. Order volume spikes. Then a few things happen at once:

- Fixed transaction charges bite harder on low AOV orders. The per-order fee hurts small baskets more than larger ones.

- International orders cost more than domestic ones. The checkout looks the same, but the economics don’t.

- You judge the store on revenue, not retained revenue. That’s how fee creep hides.

Practical rule: Review fees at the order level, not just at the monthly payout level. Profit leaks become obvious much faster.

The number that matters

Your headline revenue is vanity if your fee-adjusted order economics are weak.

Track profit per order after card fees, shipping subsidy, discounting, and returns exposure. That single view tells you whether your current pricing, payment setup, and market mix are helping the business or gradually draining it.

How Shopify Credit Card Fees Are Calculated

A customer places a $42 order. You do not keep $42. Before that money reaches your payout, card processing takes its cut, and the way that cut is built matters because it changes your profit per order.

Shopify keeps the pricing simple on the surface. Underneath, the fee is still made up of standard payment-cost components that every merchant pays in some form.

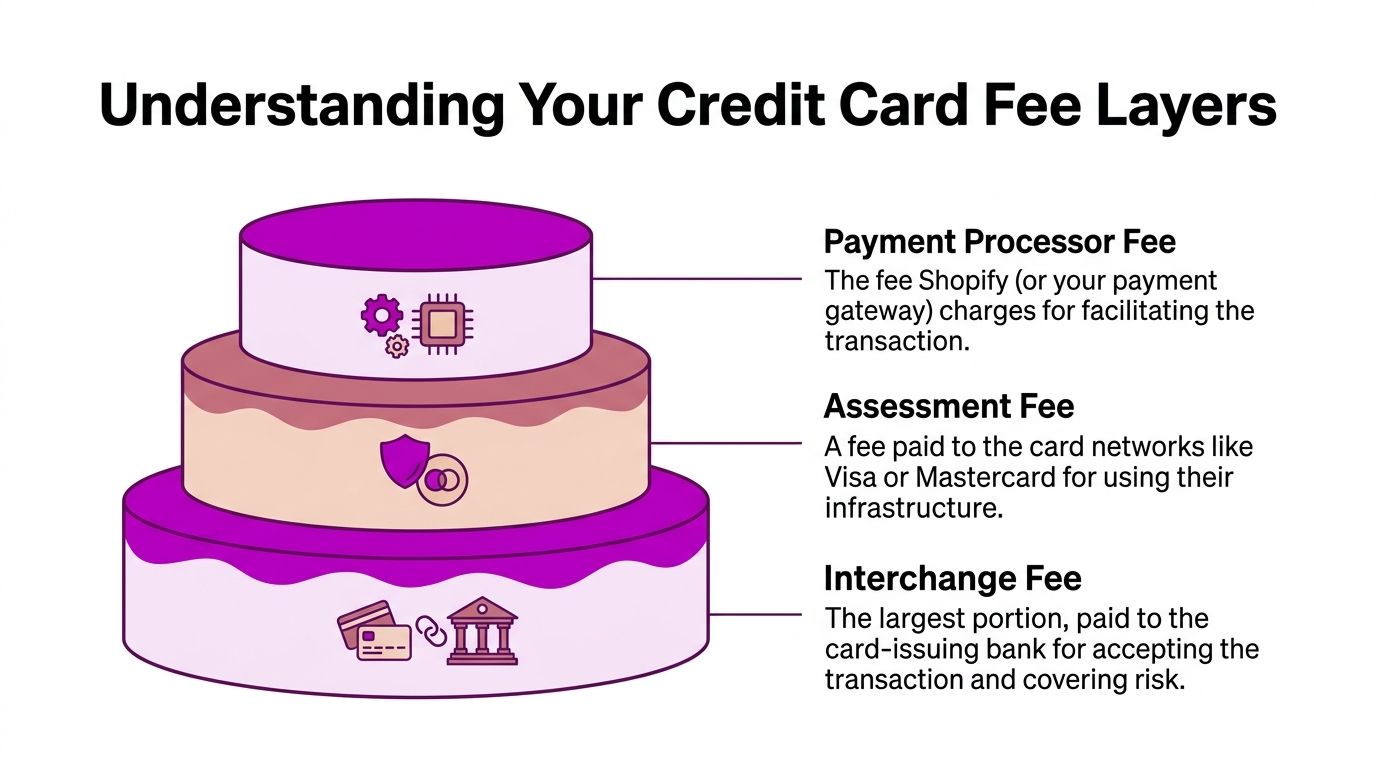

The fee has three parts

Interchange is the biggest component. It goes to the cardholder’s bank for approving the payment and taking on fraud and credit risk.

Assessment goes to the card network, such as Visa or Mastercard, for using its payment rails.

Processor markup is what the payment processor keeps for routing the transaction, running the infrastructure, and packaging the service inside your store admin.

Shopify Payments bundles those pieces into one quoted rate instead of showing them line by line.

What that means in practice

If your plan rate is a percentage plus a fixed amount per order, the fee calculation is straightforward:

Total card fee = (order value × percentage rate) + fixed fee

That formula is simple. The margin impact is not.

On a higher-ticket order, the percentage does most of the damage. On a lower-ticket order, the fixed fee takes a bigger bite out of the order. That is why two stores with the same monthly revenue can have very different payment costs if one has a lower average order value.

A quick example makes the point. If you sell a $20 item, a fixed per-order fee hits much harder than it does on an $80 order. Merchants who rely on low-AOV products, bundles with heavy discounts, or frequent flash-sale traffic usually feel this first.

Flat-rate pricing hides some detail

Shopify Payments uses flat-rate pricing. You get one published rate tied to your plan, and Shopify absorbs the complexity of interchange, card network charges, and processor markup in the background.

That convenience is useful. It also causes sloppy decision-making.

If you only look at the advertised rate, you miss the critical question. How much profit is left after payment fees on your actual order mix? That is the number to watch. A store with strong AOV and few risky transactions can live comfortably with standard rates. A store with thin margins, lots of small orders, or a high share of international buyers has less room for error.

Flat rate versus itemized pricing

Some payment setups use an itemized model, often called interchange++. In that structure, you see the underlying interchange, network assessment, and processor markup separately.

That approach gives finance teams more visibility. It also creates more statement complexity, and most Shopify merchants do not need that complexity early on.

My advice is simple. Do not obsess over the hidden plumbing unless you have enough volume for negotiation to matter. Focus first on how the current fee formula hits your contribution margin by order type, channel, and market.

The listed processing rate is not just a checkout detail. It is a variable cost that should be modeled against average order value, discount rate, shipping subsidy, and return risk.

What smart operators do with this math

Use the fee formula at the order level, not just in a monthly payout review.

Calculate net revenue after card fees for your core order types. Domestic full-price orders. Discounted orders. Subscription rebills. International orders. Once you do that, the weak spots show up fast. You will see which products can absorb your current fee structure and which ones need a pricing, bundling, or market strategy change.

Comparing Fee Rates Across Shopify Plans

The math gets practical. Shopify gives you a clear incentive to move up plans as volume grows. Lower processing rates are part of that incentive.

According to Shopify’s 2026 fee overview, domestic Shopify Payments rates are:

| Shopify Plan | Online Rate | In-Person Rate |

|---|---|---|

| Basic | 2.9% + 30¢ | 2.6% + 10¢ |

| Grow | 2.7% + 30¢ | 2.5% + 10¢ |

| Advanced | 2.4% + 30¢ | 2.4% + 10¢ |

What these plan differences mean

The percentage difference looks small on paper. On a P&L, it isn’t.

If most of your sales are online, the move from Basic at 2.9% + 30¢ to Advanced at 2.4% + 30¢ changes the economics of every single order. The fixed charge stays the same online, so the percentage reduction does the heavy lifting as revenue rises.

In-person merchants also benefit, but the online spread is where many DTC brands feel the bigger effect because card-not-present volume tends to dominate.

The right way to decide on a plan

Don’t choose a plan based on what feels “small business friendly.” Choose it based on fee-adjusted economics.

Run the calculation on your own store using three inputs:

- Your monthly card sales

- Your average order value

- Your order count

If your order volume is meaningful, even a modest reduction in the percentage rate can offset the higher plan cost. If your order count is low and your revenue is inconsistent, a higher plan may be premature.

Operating advice: Don’t ask whether a plan is “more expensive.” Ask whether the lower processing rate leaves more money after all plan costs are included.

A simple decision filter

Use this framework instead of guessing:

- Stay put if your volume is still uneven and your savings from lower card rates won’t clearly outweigh the higher plan cost.

- Move up when fee savings are predictable enough that the upgrade becomes a margin decision, not a software preference.

- Recheck quarterly because the right answer changes with growth, channel mix, and average basket size.

One more thing. If you run both online and retail, model them separately. The plan impact can look different depending on whether your business is mostly ecommerce checkout or mostly POS.

The Hidden Costs of International Sales and Chargebacks

A lot of merchants celebrate international growth before they understand what cross-border orders are costing them.

The checkout converts. Revenue looks great in the dashboard. Then the margin tells a different story. That’s because the advertised domestic rate is not the final rate on many international orders.

According to Airwallex’s breakdown of Shopify payment processing costs, Shopify adds a 1.5% fee for international transactions in the US and 2% elsewhere. The same source says currency conversion markups of 2% to 4% can stack on top, and the total fee on a cross-border sale can exceed 6%. It also notes chargeback fees of $15 to $25 per incident.

Where cross-border margin gets hit

Three leaks show up repeatedly.

- International card fees increase the cost of accepting payment from customers outside your primary market.

- Currency conversion markups take another slice when money moves across currencies.

- Chargebacks are more painful when the order already carries thinner margin from cross-border costs.

That’s why international expansion without fee modeling is sloppy. You’re not just adding reach. You’re adding payment complexity.

A bad assumption merchants keep making

Many operators still price international orders as if they behave like domestic ones. They don’t.

A cross-border sale can look profitable at gross revenue level and underperform badly once fees, FX costs, and dispute risk are included. If you’re selling internationally, you need market-level contribution margin, not one blended store margin.

If you want a clearer view of how foreign exchange costs can stack up outside Shopify too, this guide on Understanding Capitec FX costs is a useful companion for thinking through exchange-related leakage.

International growth is only good growth if the order still works after payment cost, FX drag, and dispute exposure.

Chargebacks are not just a support problem

Too many teams treat chargebacks as a customer service issue. They’re a finance issue.

Every dispute hits margin, absorbs team time, and forces you to defend revenue you thought you had already earned. If international orders are a meaningful share of your business, tighten your flows around order verification, fulfillment proof, and fraud controls. This overview of ecommerce fraud prevention best practices is worth reviewing if your dispute volume is creeping up.

The practical move is simple. Don’t look at international sales as “extra revenue.” Look at them as a separate profitability model with separate rules.

Using Shopify Payments vs a Third-Party Gateway

For most stores, Shopify Payments is the default choice for a reason. It’s integrated, simple, and operationally clean. Payouts, disputes, and payment settings live in one place. That matters.

But “default” isn’t the same as “best for every store.” In some cases, a third-party gateway is the smarter commercial decision even after the extra friction.

When Shopify Payments is the better option

If your business is straightforward, low drama, and selling in a standard retail category, Shopify Payments usually wins on simplicity alone.

You avoid the extra Shopify transaction fee that comes with external gateways, and your team has fewer systems to reconcile. For many emerging and mid-market brands, that simplicity is worth a lot because operational mess creates its own hidden cost.

When a third-party gateway deserves a serious look

This is where niche matters.

According to this explanation of Merchant Category Code impact on Shopify fees, your Merchant Category Code, or MCC, signals your industry’s risk level to card networks. High-risk niches such as digital goods or travel can face higher underlying interchange costs. The same source notes that while Shopify Payments averages this out, a specialized third-party gateway may offer better rates for low-risk niches or may be the only practical option for high-risk merchants, even with Shopify’s added transaction fee.

That means the right gateway depends on what you sell, not just how much you sell.

A practical head-to-head view

| Situation | Better fit |

|---|---|

| Standard retail brand with conventional risk profile | Shopify Payments |

| Team wants one system for checkout, payouts, and disputes | Shopify Payments |

| Niche with unusual risk profile or underwriting friction | Third-party gateway |

| Business needs processor specialization by category | Third-party gateway |

My recommendation

Start with Shopify Payments unless you have a real reason not to.

Switching to an outside gateway just because another provider advertises a lower rate is lazy analysis. If Shopify adds its own transaction fee on top, the headline savings can disappear fast. On the other hand, if your category has MCC-related friction, a specialist processor may save the business from worse approval rates, higher risk treatment, or limited support.

If you’re comparing providers in detail, this breakdown of payment gateways in Shopify is a solid place to map your options.

The smart move is to compare your actual effective cost, your approval experience, and your operational burden. Not just the sticker rate.

Practical Strategies to Reduce Your Shopify CC Fees

You have more control than you think. Most merchants leak margin on payment costs because they never build a fee strategy. They just accept the default setup and hope scale solves it.

Scale doesn’t fix bad economics. It magnifies them.

Upgrade plans when the math supports it

A lot of merchants stay on the wrong Shopify plan for too long because they fixate on subscription cost instead of total retained margin.

If your sales volume is consistent, model whether a lower processing rate on a higher plan leaves you better off after the added plan cost. Don’t guess. Pull your last few months of order count, card sales, and average basket size, then run the comparison. This is one of the easiest wins because it’s a decision you can make without changing traffic, product, or conversion.

Reduce avoidable chargebacks

Chargebacks are one of the ugliest fee leaks because they hit revenue and operating time at the same time.

Tighten your basics:

- Use clearer billing descriptors so customers recognize the charge.

- Keep proof of fulfillment organized in case a dispute lands.

- Review fraud screening settings if suspicious orders keep slipping through.

- Watch high-risk geographies and SKUs instead of treating all orders equally.

A lot of merchants spend weeks trying to raise conversion and ignore dispute prevention that would protect more profit immediately.

Best move for lean teams: Stop treating every order as equally trustworthy. Build stricter review rules around the orders most likely to become expensive.

Push healthier payment mix where possible

Not every payment path costs you the same in practice. If your store can nudge buyers toward lower-friction, cleaner payment experiences, do it.

That can mean leaning into payment methods that reduce failed payments, reduce manual support, or create a smoother checkout for trusted shoppers. The point isn’t to strong-arm customers. The point is to remove expensive friction and reduce the operational mess that follows weak payment flows.

Here’s a useful walkthrough on the broader topic:

Negotiate if you’re big enough

High-volume merchants should not assume the listed setup is the final one.

If you’re operating at meaningful scale, rate discussions become commercial discussions. That’s especially true if you’re on enterprise-grade infrastructure and processing enough volume to justify custom treatment. Merchants who never ask usually keep paying the default.

Build fee review into monthly reporting

This is the habit that separates operators from spectators.

Every month, review:

- Effective card cost by market

- Chargeback pattern by product and traffic source

- Refund and dispute exposure

- Profit per order after payment costs

Once you track fees this way, they stop being abstract overhead. They become a controllable margin lever.

Making Fee Management Part of Your Growth Strategy

The merchants who protect margin don’t treat payment costs as background noise. They treat them as part of commercial strategy.

That mindset changes everything. Instead of asking whether shopify cc fees are annoying, you ask whether each market, product line, and payment path leaves enough profit to justify the effort. That’s a much sharper way to run an eCommerce business.

The main lessons are simple. Fees are layered. Plan choice matters. International orders can be far more expensive than they first appear. Gateway choice depends on business model, not just preference. And most important, you can improve retained margin by managing this actively instead of passively.

A lot of this comes down to a broader operational discipline. If you want another useful lens on profitability, this guide on how to reduce your cost of serving pairs well with payment fee review because both force you to look past revenue and into actual delivered profit.

Review your payment reports. Model profit per order. Question every market that looks good on revenue but weak on net contribution. That’s how you turn fee awareness into a growth advantage instead of a monthly surprise.

Frequently Asked Questions About Shopify Fees

Can I avoid Shopify transaction fees entirely

You can’t avoid payment processing fees entirely. If you accept card payments, someone is getting paid to process them.

What you can avoid is Shopify’s additional transaction fee tied to using an external gateway. The usual way to avoid that extra layer is to use Shopify Payments. That’s why it’s the default for so many stores. It simplifies the setup and removes one extra source of leakage.

Can I pass credit card fees on to customers

Sometimes, but that doesn’t mean you should.

Passing fees to customers through surcharging or similar mechanisms depends on local rules and platform setup. Even where it’s allowed, it can hurt conversion and create checkout friction right at the point where the customer is about to pay. For most consumer brands, that tradeoff is ugly. You might recover some fee cost and lose more in abandoned checkout or lower customer trust.

My advice is blunt. Most stores should fix the economics behind the scenes before they start making checkout feel punitive.

Are Shopify Plus credit card fees negotiable

For higher-volume merchants, yes. That’s one of the strategic advantages of operating at the upper end of the Shopify ecosystem.

If your business is processing enough volume, payment terms become something to discuss, not just accept. Merchants often leave money on the table because nobody owns the negotiation. Finance assumes ecommerce handles it. Ecommerce assumes finance handles it. Then nothing happens and the default pricing stays in place.

If you’re large enough to have leverage, use it. Payment rates are not an area where serious operators stay passive.

What should I check first if fees feel too high

Start with the obvious suspects:

- Your current Shopify plan and whether it still fits your sales profile

- Your market mix, especially how much revenue comes from international cards

- Your chargeback pattern and whether specific products or channels drive disputes

- Your payment setup, including whether a different gateway structure would help

Don’t start by chasing tiny optimizations. Start by finding the largest leak.

If your margins feel tighter than your revenue suggests, ECORN can help you audit the actual profit impact of payment fees, plan choice, checkout setup, and cross-border complexity. We work with Shopify brands that want cleaner economics, stronger conversion, and a store that scales without fee drag eating the gains.

Shopify Add to Cart Button: A Practical 2026 Guide

Customer Feedback Automation: A Practical eCommerce Guide

Critical Rendering Path: A Guide for Shopify Stores

How to Promote on TikTok for eCommerce in 2026

B2B eCommerce Consulting That Drives Real Revenue

10 Best Practices for Site Navigation in 2026

Return vs Refund for Shopify Stores: A Practical Guide

What Is Customer Lifetime Value and Why It Matters

What Is Voice of Customer Research for eCommerce

SMS Marketing for Ecommerce That Actually Converts

Master How to Improve Email Deliverability in 2026

Top 7 eCommerce Partners NYC for Shopify Brands in 2026

Machine Learning for Ecommerce: Boost Your Shopify Store

Beauty Market Research: Your 2026 Growth Guide

Shopify International Expansion: A 2026 Roadmap

What Does CRO Stand for in Business: Understanding CRO

Shopify Visual Merchandising: A Playbook for Higher Sales

Shopify Landing Page Design: Master Conversion in 2026

10 Best AI SEO Optimization Tools for Shopify in 2026

Agentic AI for Ecommerce: Boost Your Sales in 2026

Mastering Email Marketing Data for eCommerce Growth

Conversion Rate Optimisation Australia: Boost Your Sales

Conversion Rate Optimization AI: Your Shopify Store Guide

10 Product Bundling Strategies for Shopify in 2026

How to Increase Customer Lifetime Value: A Shopify Playbook

AI Customer Service Automation: Shopify Guide 2026

Clean Website Design: A Shopify Conversion Playbook

Omnichannel Retail Strategy: A Shopify Playbook

Product Data Enrichment: A Guide for Shopify Brands

Instagram Shopping Features a Guide for Shopify Stores

What Is Revenue Optimization: A Holistic RevOps Guide

Benefits of Conversion Rate Optimization: Boost Your

WordPress to Shopify Migration: Your 2026 Seamless Switch

Boost Sales: Ecommerce Payment Processing Guide 2026

Unified Commerce Platform: Benefits, KPIs & Shopify Guide

How to Reduce Bounce Rate eCommerce: Your 2026 Guide

Shopify API Integration: A Practical End-to-End Guide

How to Implement Data Governance: A 2026 Guide

Shopify Store Development Cost: A 2026 Breakdown

What Is Server Side Tracking: The Shopify Guide 2026

Marketing Automation Workflows: A Shopify Guide for 2026

Shopify: How to Reduce Technical Debt

Shopify UX Design Change: A Playbook for Growth

User Generated Content Strategy: Shopify Playbook

Shopify Pause and Build Plan Cost: A Complete 2026 Guide

Compare at Price on Shopify: A Complete Guide for 2026

Where Can I Sell My Prints? 10 Best Platforms for 2026

Shopify Order Management System: The Ultimate Guide 2026

What Is Marketing Attribution? an eCommerce Guide for 2026

10 Best Black Friday Sales Sheets for 2026

Discover the Top Social Media Marketing Agencies For

Consumer Confidence Definition for eCommerce in 2026

What Is Social Commerce? Your 2026 Guide to Boosting Sales

A Social Ad Campaign Playbook for eCommerce Growth

7 Best FAQ Page Examples for SaaS & eCommerce

Market Research in Fashion Industry: A Guide for Shopify

Shopify Migration Services: Expert Guide for 2026

Mastering FB Retargeting Ads for Shopify in 2026

What Is Omnichannel Ecommerce

Master Your Shopify Plus Migration: The 2026 Guide

Shopify Integration Services: A Merchant's 2026 Guide

Shopify Collection Description: A Guide to SEO & Sales

Shopify Plus Contact: Reach Sales & Support Effectively

Top Luxury Shopify Stores: Design & UX Strategies

How to Improve Customer Experience: A Shopify Roadmap

Creative Facebook Ads: 10 Examples for Shopify Brands

Remarketing with Facebook Ads: A Shopify Guide for 2026

SEO Linking Strategies for Shopify Stores

Top 7 Statistics YouTube Channels for eCommerce in 2026

Hiring Shopify Plus Designers: A Founder's Guide

Shopify Product Variation: Master Your Variants for 2026

Leverage Ai Solutions Brands: Your 2026 Shopify Growth Guide

Filters in Shopify: A Guide for Growing Brands

Shopify Plus Developer: A Guide for Growing Brands

When Does Black Friday Online Start? A 2026 Guide

Black Friday Email Marketing: Shopify & Klaviyo Guide

Polaris Design System: The Complete Shopify Guide

How to Hire a Consultant Email Marketing Expert

What Is Q4? A Shopify Merchant's Guide to Peak Season

Marketing Organization Structure for eCommerce Growth

Top Account-Based Marketing Agency Guide for 2026

7 Remarketing Ad Examples for Your 2026 Campaigns

AI Retail Solutions: Boost Your Shopify Store

Migrate to Shopify: The Definitive 2026 Guide

Shopify Authentication App: A Guide for Secure Stores

Why Strategic Marketing Is Important for Growth in 2026

How to Create a Size Chart in Shopify: 2026 Guide

Shopify Themes for Jewelry: The Definitive 2026 Guide

Minimal Shopify Templates: Faster, Higher-Converting Stores

Best Shopify Apps for Beginners in 2026

How to Improve Online Shopping Experience in 2026

Shopify Design and Development Services: A 2026 Guide

Small Business Social Media Marketing Agency: A Hiring Guide

Bulk Edit Shopify: A Guide to Save Hours on Store Updates

2026 Trends in Food and Beverage Industry

Post Purchase Survey Guide for Shopify Stores

How to Build an Ecommerce Brand in 2026

Conversion Rate Optimization for Ecommerce: Maximize Profit

How to Use Customer Data to Increase Sales: A Guide

Shopify for Enterprise: The 2026 Deep Dive Guide

newsletter in your inbox