You're probably in one of two situations right now.

Either sales are growing and your deposits still look smaller than they should, or conversion has flattened and you've already tested the obvious things like product pages, offers, and email flows. In both cases, the checkout stack is usually carrying more weight than founders expect.

Most brands treat payments like plumbing. Set up Stripe or Shopify Payments, make sure cards go through, then move on. That's fine when volume is low. It stops being fine when payment fees start eating margin, false declines block real customers, or an international shopper lands at checkout and hesitates because the experience doesn't feel local.

Ecommerce payment processing isn't just how money moves. It shapes whether customers trust your checkout, whether transactions get approved, and how much revenue you keep after each order. That makes it a conversion problem as much as an operations problem.

Why Payment Processing Is Your Unseen Growth Engine

A lot of founders first notice payment processing when the payout report doesn't match store revenue. Orders look healthy in Shopify. The bank account says otherwise. Then the finance team points at fees, reserves, disputes, and settlement timing, while the growth team points at checkout abandonment and low authorization rates.

Both teams are looking at the same system from different angles.

Why founders underestimate payments

The common mistake is to think payment processing starts after the sale. It doesn't. It starts when the buyer asks a silent question at checkout: Do I trust this enough to pay?

That decision gets shaped by small details:

- Payment method fit: If the buyer wants Apple Pay, PayPal, a local wallet, or BNPL and you don't offer it, friction shows up immediately.

- Security experience: If the checkout feels risky or the fraud flow is clumsy, good customers leave.

- Pricing structure: If your processor's pricing model is wrong for your volume, every order becomes less profitable.

- Settlement reliability: If funds arrive unpredictably, inventory planning and cash flow both get harder.

A good setup removes doubt. A bad one adds just enough hesitation to cut conversion without giving you a clear warning.

Where payment choices hit revenue

The growth effect is practical, not theoretical.

If checkout is smooth, customers finish. If security is modern, more legitimate transactions get approved. If wallets and local payment methods are available, the payment step feels familiar instead of risky. If fees are structured well, you keep more contribution margin from every campaign you already paid to acquire.

Practical rule: Treat payment processing as part of CRO, not just finance ops.

That means reviewing payments the same way you review landing pages. Look at where people stall, what gets declined, what payment methods get used, how long funds take to settle, and which fees are compounding as order count rises.

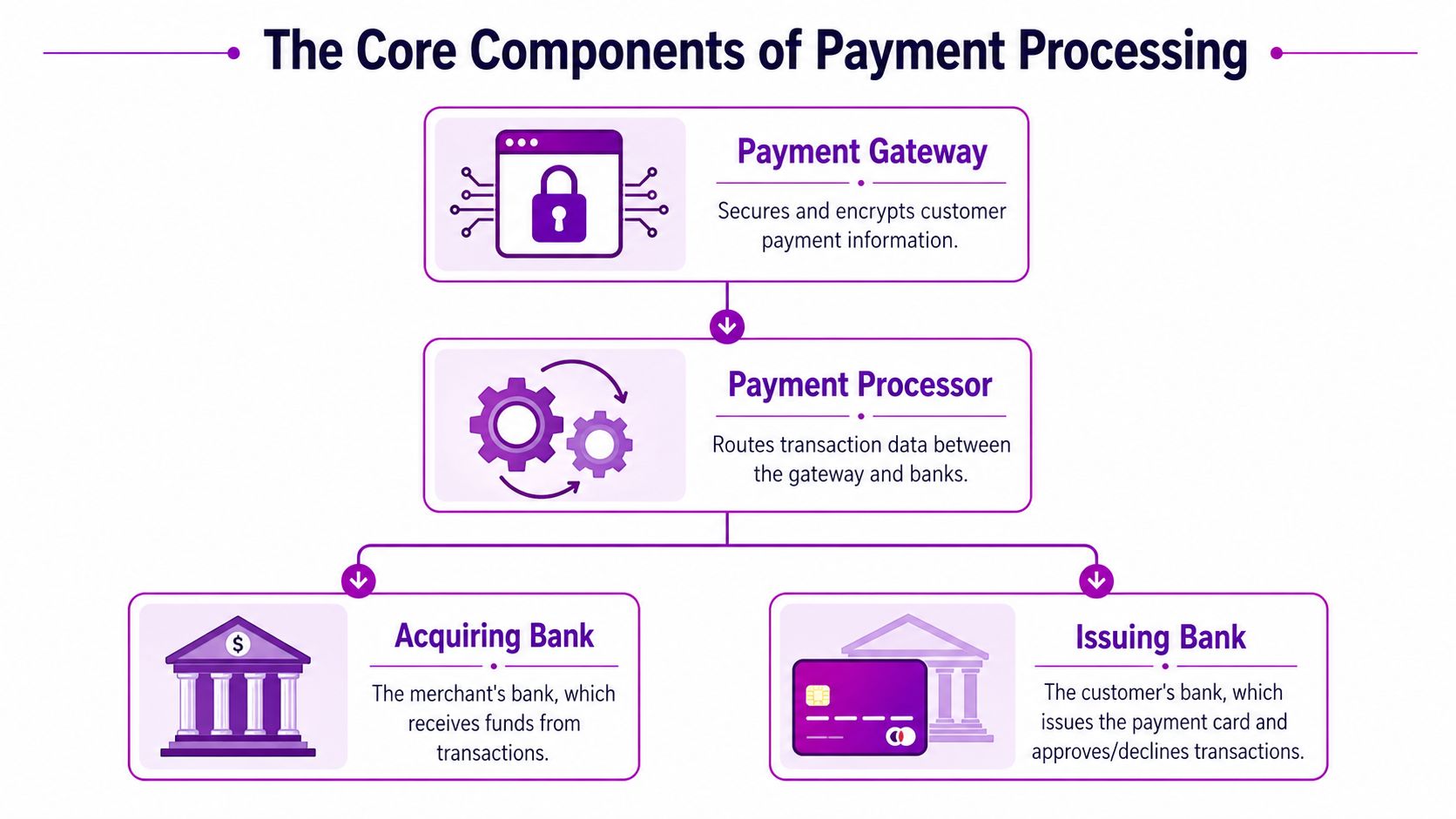

The Core Components of Payment Processing

Most confusion around ecommerce payment processing comes from lumping everything together as “the payment provider.” In reality, several jobs are happening at once.

A simple analogy helps. Think of checkout like a restaurant.

The payment gateway is the host at the front. It greets the customer's payment details, secures them, and passes them inside. The payment processor is the kitchen. It takes the order, routes it to the right places, and makes sure the transaction gets handled correctly. The merchant account is the cash drawer. It temporarily holds the funds before they land in your business bank account.

What each component actually does

Payment gateway

The gateway handles the customer-facing handoff of payment data. It encrypts card or wallet information and sends it securely for approval.

If checkout forms, wallet buttons, and payment data capture are the front door, the gateway is that door. When the door is clunky, users feel it immediately.

Payment processor

The processor does the routing work in the background. It communicates with the merchant side, card networks, and banks so the transaction can be approved or declined.

This is where speed, reliability, fraud logic, and integrations matter. A processor that's technically strong can improve approval quality and reduce avoidable checkout failures. A weak one can turn normal purchasing behavior into failed transactions.

Merchant account

The merchant account is where approved funds sit before settlement reaches your bank. Some businesses use a dedicated merchant account setup. Others use a provider that bundles this into one service.

The timing of cash flow directly affects operations. If payouts are delayed, the issue usually isn't your product sales. It's the path money takes after authorization.

Why all-in-one platforms feel simpler

Providers like Stripe and Shopify Payments often combine gateway, processing, and merchant account functionality into one stack. That's why setup feels fast. For many brands, that simplicity is worth a lot.

The trade-off is control. Bundled systems are easier to launch, but they can be less flexible when you want custom routing, deeper cost optimization, or more control over risk settings.

The practical difference for a growing brand

When you understand these layers, vendor conversations get much clearer. You stop asking, “What are your fees?” and start asking better questions:

- Gateway questions: How smooth is checkout on mobile? Which wallets and local methods are native?

- Processor questions: How are declines handled? What fraud controls are built in?

- Merchant account questions: How often are funds settled? Are reserves or holds likely for our business model?

If you sell both online and in physical environments, the same principles apply. Vendmoore's latest vending machine guide is useful because it shows how contactless payment design affects trust and speed even outside a traditional ecommerce cart. The customer expectation is the same. Pay fast, feel safe, move on.

The best payment stack is the one customers barely notice and operators can fully understand.

How a Transaction Travels from Cart to Bank Account

A customer clicks “Pay now,” sees a confirmation message, and assumes the money has arrived. It hasn't. At that moment, the transaction has only started its trip.

This is why founders get confused by statuses like authorized, captured, pending, paid out, and settled. They sound interchangeable. They're not.

Authorization comes first

Start with one order. A shopper enters card details or uses a wallet like Apple Pay. Your gateway encrypts that data and sends it into the payment chain. The processor routes it through the merchant side and toward the customer's issuing bank.

At this point, the bank checks basics. Is the card valid? Are funds or credit available? Does the transaction look risky?

If the answer is yes, the bank authorizes it. That doesn't mean you've been paid. It means the bank has approved the request to charge.

Capture turns approval into a charge

After authorization, the transaction has to be captured. Some stores capture immediately. Others delay capture until shipment or fulfillment.

That distinction matters. If authorization is the customer saying, “You may charge me,” capture is the moment you do it.

Brands that sell pre-orders, custom items, or delayed-ship inventory need to understand this well. If you wait too long, an authorization can expire and you'll need to request approval again.

Here's a simple visual explainer for teams that need to train staff or stakeholders on the flow:

Clearing and settlement are where cash timing appears

Once captured, the payment enters clearing and settlement. This is the behind-the-scenes accounting movement between institutions. The issuing bank releases funds through the network path, and the acquiring side receives them before they're transferred into your merchant account and then your bank account.

This is why payout timing can lag behind order volume. Your store may say “paid,” but your finance team is still waiting for the funds to complete the settlement path.

Why this matters operationally

Founders usually care about this flow for three reasons:

- Cash forecasting: Marketing can scale faster than payouts arrive.

- Support issues: Customers see a bank hold and ask why an order wasn't completed.

- Ops debugging: A transaction can be approved but not captured, or captured but not yet settled.

If you don't know where a transaction is in the lifecycle, you can't diagnose revenue leakage accurately.

A clean payment operation maps order states to money states. That sounds basic, but it prevents a lot of expensive confusion between growth, support, finance, and fulfillment teams.

Decoding Payment Processing Fees and Hidden Costs

Most brands know they're paying for payment processing. Fewer know exactly what they're paying for.

That's where margin erodes. The headline fee might look acceptable, but the actual cost structure can be much heavier once you factor in transaction mix, order value, and volume.

According to Forbes Advisor's explanation of interchange-plus pricing, the dominant ecommerce payment processing model is 2.9% + $0.30 per transaction, and switching to interchange-plus pricing can reduce total processing costs by 10% to 15% for businesses with over $5M in annual revenue.

What's inside the fee

A payment fee isn't one thing. It usually includes three layers:

- Interchange: The portion paid to the issuing bank.

- Assessment: The portion paid to the card network.

- Processor markup: The amount your payment provider adds.

The problem isn't that these costs exist. The problem is that many merchants only see the blended outcome and never question whether their pricing model still fits their scale.

Payment Processing Pricing Models Compared

| Pricing Model | Best For | Pros | Cons |

|---|---|---|---|

| Flat-rate | Early-stage brands, simpler operations | Easy to understand, predictable billing, fast setup | Can become expensive as volume grows |

| Interchange-plus | Brands with larger revenue and tighter margin control | More transparent, often better for high volume, easier to audit | More complex statements, requires closer review |

| Tiered | Merchants who accept provider-defined pricing buckets | Can look simple at first glance | Usually less transparent, harder to benchmark, easy to overpay |

Why flat-rate is convenient and expensive

Flat-rate pricing wins on speed. You can forecast it quickly and hand it to accounting without much explanation. That's why it's common for newer brands.

But it hides variation. If your business has healthy average order value or significant payment volume, the convenience premium can become costly. At that point, what felt “simple” starts acting like a tax on growth.

The flat fee changes the economics of low-value orders

The fixed transaction component matters more than is commonly understood. On lower-value purchases, that flat fee takes a bigger bite out of contribution margin.

That's why payment strategy isn't separate from merchandising. Product bundles, minimum order thresholds, and subscription structures all interact with processing cost.

Margin check: A processor decision that looks minor on a rate card can materially change the profitability of your lowest-priced products.

Hidden costs usually show up outside the headline rate

Founders often focus on the visible transaction fee and miss the operational leakage around it. Watch for:

- Chargeback handling costs: Even when the dispute itself matters more than the fee, these costs add up.

- Cross-border complexity: International payments can create extra cost and reconciliation work.

- Accounting friction: If payout data is messy, finance spends more time cleaning it.

That last point matters more as the business grows. If your team is trying to reconcile payout timing, refunds, and fee breakdowns, a clean accounting workflow matters just as much as the processor itself. A practical example is this guide on linking Stripe payments to Xero, which shows how payment data quality affects downstream finance work.

The right pricing model doesn't just lower fees. It makes profitability easier to see.

Mastering Security Compliance and Fraud Prevention

Security is where many ecommerce brands make a costly trade by accident. They either tighten fraud rules so aggressively that real customers get blocked, or they relax controls and pay for it later through disputes, support tickets, and lost trust.

The better approach is to treat security as part of conversion design.

PCI compliance is basic checkout hygiene

If you accept card payments, PCI DSS compliance is not optional. It's the standard that governs how card data is handled and protected.

For Shopify merchants, the practical question usually isn't whether compliance matters. It's how much of the burden your platform and payment setup absorb for you. This guide on PCI compliance for Shopify stores is a useful reference if you need the operational side explained clearly.

Compliance protects the business. Of greater significance, it supports the customer's willingness to complete the payment. Shoppers may never mention PCI by name, but they feel the presence or absence of trust instantly.

Why 3D Secure 2 matters now

Modern fraud prevention can't rely on blunt rules alone. That's why 3D Secure 2.0 has become so important.

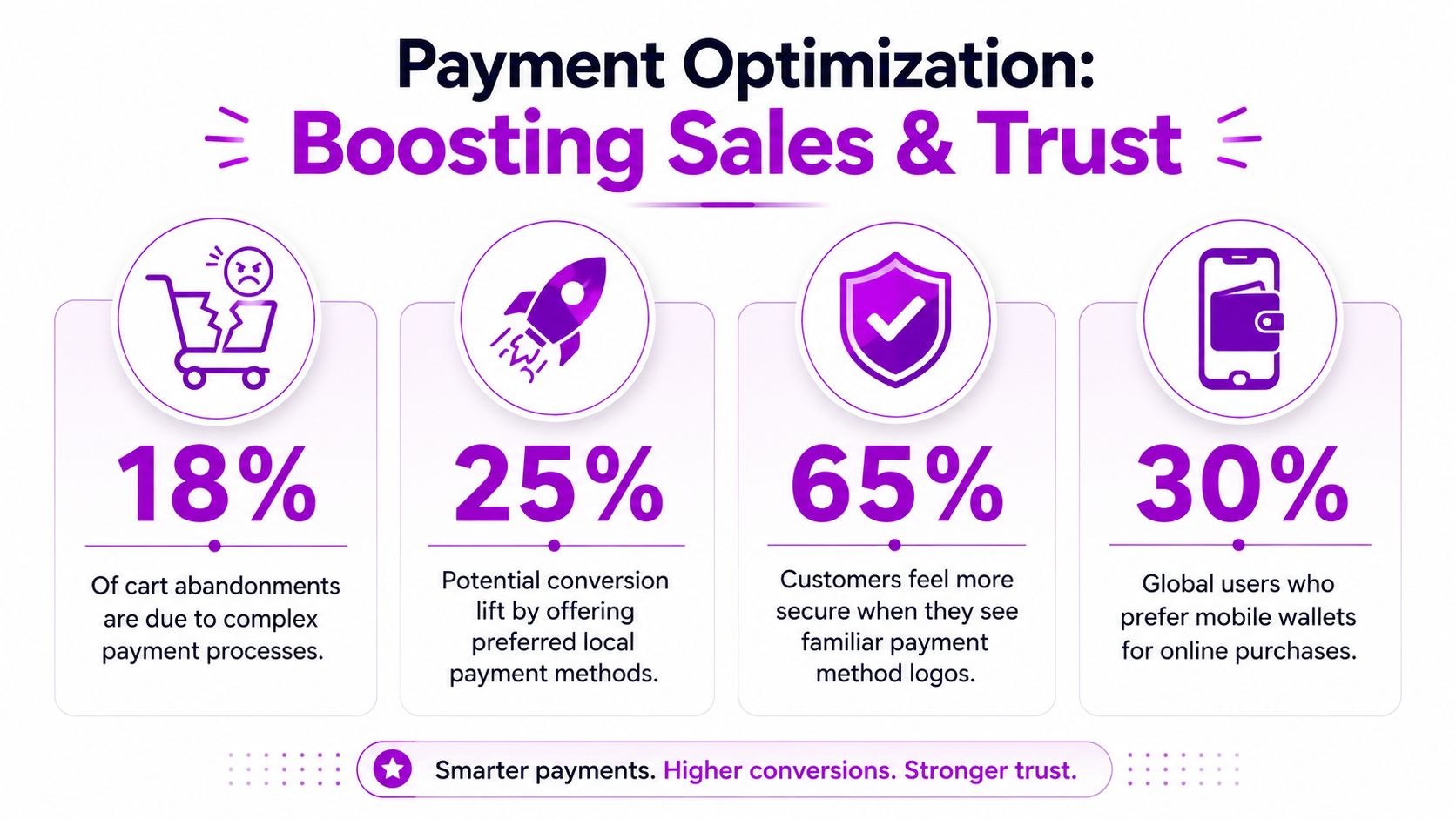

According to Stripe's 3D Secure documentation, 3DS2 uses biometric authentication to reduce fraud by up to 70% while maintaining 99% authorization rates, and merchants adopting it see a 25% reduction in payment rejection rates due to false-positive fraud flags.

That combination matters because it solves the classic checkout tension. You want stronger fraud protection, but you don't want more friction. Legacy approaches often forced a hard trade. 3DS2 is built to reduce that trade.

What good fraud prevention looks like in practice

Strong setups usually combine several layers rather than one dramatic filter.

- Tokenization: Sensitive payment details are replaced with secure tokens, which lowers exposure and supports safer repeat purchases.

- Adaptive verification: Extra checks should appear when risk is high, not on every order.

- Behavioral monitoring: Good systems evaluate transaction patterns, not just static rules.

- Manual review discipline: Human review should catch edge cases, not become a bottleneck for normal orders.

What doesn't work

Rigid fraud rules often create a different kind of loss. Teams celebrate fewer risky orders while ignoring the legitimate customers who never made it through checkout.

Common examples include blocking mismatched billing and shipping details too aggressively, challenging returning customers who changed devices, or treating every international order as suspicious.

Security should remove bad actors without making good customers prove they belong.

That's why payment teams and CRO teams need to work together. If the fraud tool is set by finance or operations alone, it often over-weights risk. If it's set by growth alone, it often under-weights exposure. The right balance protects revenue from both sides.

How Payments Drive Conversion and Customer Trust

If you want a cleaner way to think about checkout, use this rule: every payment choice either reduces doubt or creates it.

That's why payment setup belongs in CRO conversations. It affects not only whether the customer can pay, but whether they feel comfortable paying right now, on this device, in this market, with this level of trust.

Familiar methods reduce hesitation

Customers don't want to stop and interpret your checkout. They want to recognize it.

According to BlueSnap's payment method statistics, digital wallets are projected to account for 54% of global ecommerce transaction value by 2026, and 93% of global consumers say pricing in their local currency significantly affects their purchase decision.

Those two facts point to the same conversion lesson. Familiarity closes sales.

If a shopper sees Apple Pay, Google Pay, PayPal, or a local wallet they already trust, the checkout feels shorter. If they see local currency, the price feels more certain. Remove that familiarity and you add cognitive work at the moment you should be removing it.

Shopify Payments versus external gateways

For many Shopify brands, Shopify Payments is the simplest default because it reduces setup complexity and keeps the checkout stack native. That's often the right call for speed, reporting cohesion, and operational simplicity.

But there are cases where an external gateway makes sense:

- International expansion: You may need stronger local method coverage.

- Complex risk profiles: Certain businesses need more customized fraud handling.

- Market influence: Mature brands may want more flexibility around pricing or routing.

The mistake is thinking “native” is always best or “custom” is always advanced. The right answer depends on whether your current setup is improving conversion or merely functioning.

Wallets and local methods are CRO tools

Digital wallets don't win because they're trendy. They win because they remove typing, reduce hesitation, and piggyback on trust customers already have with their device or provider.

Local payment methods do the same job in international markets. They tell the shopper, “This store understands how people like you pay.” That matters.

For teams already working on broader conversion improvements, Fundl's guide to growth is a good complement because it frames conversion work as a system, not a single page-level fix. Payments belong in that system.

The practical CRO view of checkout

When reviewing payments, don't ask only whether transactions process. Ask:

- Do mobile shoppers have a one-tap path?

- Do international visitors see a local-feeling checkout?

- Do payment logos reinforce trust before hesitation starts?

- Are returning customers able to pay without repeating work?

The highest-converting checkout usually feels obvious, not impressive.

That's the right bar. If the payment step feels effortless, trust is doing its job.

Your Checklist for Choosing the Right Payment Partner

By the time a brand starts reviewing payment providers seriously, the wrong questions usually dominate the conversation. Teams compare brand names, headline fees, or feature lists. Those matter, but they don't tell you whether the provider will help conversion, preserve margin, and support scale.

A better selection process looks at fit.

According to Uniteller's overview of major payment processors, PayPal commands nearly 46% of global online payment processing, followed by Stripe at 17.33% and Shopify Pay Installments at 15.73%. Market share tells you which platforms are widely used. It doesn't tell you which one is right for your store.

Use this checklist before you sign

Security and risk controls

Ask how the provider handles PCI scope, tokenization, fraud review, and 3DS2 support. If the answer is vague, that's a warning.

You need security that protects revenue without choking approval rates.

Payment method coverage

Check whether the provider supports the methods your customers want to use, not just the methods your team is used to seeing.

That includes cards, wallets, and relevant local methods for the markets you serve.

Pricing transparency

Look beyond the headline rate. Ask for a clear explanation of markup, extra fees, dispute costs, and any volume-based changes.

If pricing requires too much interpretation before you've even signed, reporting will likely be worse after go-live.

Integration quality

A processor can be technically capable and still painful in practice. Review how it connects with your platform, checkout, subscriptions, ERP, and finance tools.

If you're evaluating implementation trade-offs in more depth, this payment gateway integration guide is useful for mapping what a clean deployment should look like.

The questions operators should ask

Use vendor calls to pressure-test reality, not just collect demos.

- What happens when a legitimate order is incorrectly flagged?

- How are payouts timed, and what can delay them?

- Which payment methods are strongest in our target countries?

- How much control will we have over checkout behavior and fraud settings?

- What support do we get when approval rates drop or disputes rise?

What the right partner feels like

The right provider usually creates calm. Finance can reconcile quickly. Growth can trust the checkout. Support can explain payment issues clearly. Operations can forecast cash with fewer surprises.

The wrong one creates recurring ambiguity. Orders process, but nobody feels fully in control of why some fail, why fees drift upward, or why expansion into new markets suddenly gets complicated.

Choose the payment partner that makes revenue easier to convert, protect, and understand.

That's a better lens than feature comparison alone. Payments sit at the intersection of trust, conversion, and cash flow. The partner you choose affects all three.

If your Shopify store is growing and your payment setup still feels like a black box, ECORN can help you turn it into a conversion asset. Their team works with brands on Shopify development, CRO, and scalable ecommerce execution, so payment experience, checkout performance, and growth strategy support each other instead of fighting for priority.

Unified Commerce Platform: Benefits, KPIs & Shopify Guide

How to Reduce Bounce Rate eCommerce: Your 2026 Guide

Shopify API Integration: A Practical End-to-End Guide

How to Implement Data Governance: A 2026 Guide

Shopify Store Development Cost: A 2026 Breakdown

What Is Server Side Tracking: The Shopify Guide 2026

Marketing Automation Workflows: A Shopify Guide for 2026

Shopify: How to Reduce Technical Debt

Shopify UX Design Change: A Playbook for Growth

User Generated Content Strategy: Shopify Playbook

Shopify Pause and Build Plan Cost: A Complete 2026 Guide

Compare at Price on Shopify: A Complete Guide for 2026

Where Can I Sell My Prints? 10 Best Platforms for 2026

Shopify Order Management System: The Ultimate Guide 2026

What Is Marketing Attribution? an eCommerce Guide for 2026

10 Best Black Friday Sales Sheets for 2026

Discover the Top Social Media Marketing Agencies For

Consumer Confidence Definition for eCommerce in 2026

What Is Social Commerce? Your 2026 Guide to Boosting Sales

A Social Ad Campaign Playbook for eCommerce Growth

7 Best FAQ Page Examples for SaaS & eCommerce

Market Research in Fashion Industry: A Guide for Shopify

Shopify Migration Services: Expert Guide for 2026

Mastering FB Retargeting Ads for Shopify in 2026

What Is Omnichannel Ecommerce

Master Your Shopify Plus Migration: The 2026 Guide

Shopify Integration Services: A Merchant's 2026 Guide

Shopify Collection Description: A Guide to SEO & Sales

Shopify Plus Contact: Reach Sales & Support Effectively

Top Luxury Shopify Stores: Design & UX Strategies

How to Improve Customer Experience: A Shopify Roadmap

Creative Facebook Ads: 10 Examples for Shopify Brands

Remarketing with Facebook Ads: A Shopify Guide for 2026

SEO Linking Strategies for Shopify Stores

Top 7 Statistics YouTube Channels for eCommerce in 2026

Hiring Shopify Plus Designers: A Founder's Guide

Shopify Product Variation: Master Your Variants for 2026

Leverage Ai Solutions Brands: Your 2026 Shopify Growth Guide

Filters in Shopify: A Guide for Growing Brands

Shopify Plus Developer: A Guide for Growing Brands

When Does Black Friday Online Start? A 2026 Guide

Black Friday Email Marketing: Shopify & Klaviyo Guide

Polaris Design System: The Complete Shopify Guide

How to Hire a Consultant Email Marketing Expert

What Is Q4? A Shopify Merchant's Guide to Peak Season

Marketing Organization Structure for eCommerce Growth

Top Account-Based Marketing Agency Guide for 2026

7 Remarketing Ad Examples for Your 2026 Campaigns

AI Retail Solutions: Boost Your Shopify Store

Migrate to Shopify: The Definitive 2026 Guide

Shopify Authentication App: A Guide for Secure Stores

Why Strategic Marketing Is Important for Growth in 2026

How to Create a Size Chart in Shopify: 2026 Guide

Shopify Themes for Jewelry: The Definitive 2026 Guide

Minimal Shopify Templates: Faster, Higher-Converting Stores

Maximize Profit: Shopify CC Fees 2026 Guide

Best Shopify Apps for Beginners in 2026

How to Improve Online Shopping Experience in 2026

Shopify Design and Development Services: A 2026 Guide

Small Business Social Media Marketing Agency: A Hiring Guide

Bulk Edit Shopify: A Guide to Save Hours on Store Updates

2026 Trends in Food and Beverage Industry

Post Purchase Survey Guide for Shopify Stores

How to Build an Ecommerce Brand in 2026

Conversion Rate Optimization for Ecommerce: Maximize Profit

How to Use Customer Data to Increase Sales: A Guide

Shopify for Enterprise: The 2026 Deep Dive Guide

Email Marketing Agencies: The Guide for Shopify Brands

Boost Sales With The Right Shipping Shopify App

Your Guide to the Shopify Site Map

7 Headless Commerce Examples for 2026

Mastering Trends in Cosmetic Industry for 2026

Transfer Shopify to BigCommerce The Complete 2026 Playbook

What Is Shopify Collective? Your 2026 Guide to Success

Unlock Shopify Growth with Site Link SEO

Integrating Shopify and WordPress A Complete Guide for 2026

Naming a Clothing Store: A Shopify Founder's Playbook

Guide to buying shopify store in 2026

Buying shopify store: Buying a Shopify Store: Invest Wisely

Food & Beverage Marketing: A Complete Guide for 2026

Facebook Ads Agency: A Shopify Brand's Hiring Guide

Shopify Apparel Stores: A 2026 Launch & Scale Guide

How to Deactivate Shopify Store: The 2026 Guide

Shopify and Square: The 2026 Ultimate Comparison

Your Guide to Beauty Products Ecommerce

A Guide to Marketing for Beauty Brands in 2026

Your Guide to Facebook Black Friday Ads

Facebook Ad Ecommerce for Shopify Growth

Iconography Web Design The Definitive Guide for Shopify Stores

A Modern Backlinks SEO Strategy for Shopify Stores

How to Launch an Online Store: A Step-by-Step Success Guide

Optimize Shopify Store: Master Performance in 2026

Successful Migration for Shopify: Protect SEO & Grow

Maximize Traffic & Sales: Get Your Free Website Audit Report

Master the Best Ads Facebook Formats for eCommerce Success

How to Find the Best Ecommerce Agency Near Me in 2026

10 Crucial White Hat Techniques SEO for Shopify in 2026

How to Reduce Returns and Boost Profits in Your eCommerce Store

What Is Ecommerce Personalization A Guide to Unlocking Growth

Payment gateways in shopify: The Ultimate Guide for Merchants 2026

newsletter in your inbox